The Journal of Digital Assets

- Volume 1

- December 2022

- Issue 1

- Stablecoin as a Catalyst for DeFi Ecosystem Expansion

- Gongpil Choi

- First Published: 05 December 2022

- Abstract | Full Text(633) | PDF download(225)

Content (Full Text)

Stablecoin as a Catalyst for DeFi Ecosystem Expansion |

||||||||||||||||||||||||||||||||||||||||

Abstract |

||||||||||||||||||||||||||||||||||||||||

This paper explains a new breed of stablecoin specifically designed for decentralized finance (DeFi) ecosystem expansion. It differs from earlier versions by specifically addressing the needs of DeFi participants, who constantly face frictions related to volatility, slippage, and forced liquidation. The so-called DeFi stablecoin is designed specifically to satisfy critical requirements for promoting the DeFi ecosystem by providing reduced volatility, improved capital efficiency, and better decentralization over a long-term period of time. Unlike other protocols for cross-border payment and value transfer, the current version tries to achieve the required stability of native protocol tokens, which act as catalysts for liquidity provision within the ecosystem. A grassroots DeFi stablecoin using the native protocol token requires the combinatorial use of centralized stablecoin, e.g., USDC, with specific choice parameters over volatility, slippage, and expected return. The eclectic approach to secure better liquidity instruments for DeFi depends on the use of fiat-backed stablecoin as a pillar to stabilize any native token with good disclosure and transparency. A preliminary empirical study shows that the current approach reduces volatility, allows more capital-efficient market transactions, and makes the financial system more resilient to different shocks. And future studies need to find whether this hybrid approach can serve as a prudential supervisory guideline for the DeFi ecosystem and embrace the multi-collateral mix. Keywords: Decentralization, DeFi, stablecoin, tokenomics. |

||||||||||||||||||||||||||||||||||||||||

| I. INTRODUCTION | ||||||||||||||||||||||||||||||||||||||||

WHILE cryptocurrency has the potential to massively upgrade the effectiveness of money, it is highly volatile in nature and hence prevents itself from acting as a medium of exchange or store of value [5], if not for liquidity pool (LP) staking in DeFi. The emerging consensus is that the development of stable cryptocurrencies will enable it to function as a medium of exchange, a store of value, and method of payment in this potentially thriving ecosystem. To economists, the benefits of stablecoin include lower-cost, safe, realtime, and more competitive payments compared to what consumers and businesses experience today. It is also the relevant incentive mechanism for distributed and decentralized environments since it simultaneously captures stability of the legacy world and the interoperability of the crypto space. Specifically, stablecoins could rapidly make it cheaper for businesses to accept payments and allow governments to run conditional cash transfer programs (including sending Covid-19 stimulus money). And they could further connect unbanked or underbanked segments of the population by offering token alternatives to siloed account-based system. Stablecoins are vital to explore interesting applications in DeFi, an enabler to expand the world of decentralized finance. Even with all these potential benefits for all, stablecoins have become the center of public scrutiny for such compliance issues as tax and AML-KYC requirements. As expounded by the Treasury secretary, Janet Yellen, in a recent speech [20], both the opportunities and challenges of stable cryptocurrencies seem well-established. Besides various concerns and mixed views on stablecoins, its vital function to engage with DeFi is crucial because they conveniently separate the risk/return calculus of the DeFi services from the high volatility of digital assets. Interoperability requires stable prices for value exchange and investors expect a steady unit of account for financial services. Stablecoins are closer to addressing the various needs of digital world by offering better stability in an interconnected setting. In principle, the expanded trust base of stablecoin based on a mix of eligible collaterals is identifiable and the Treasury operations ensure dynamic stability over time. |

||||||||||||||||||||||||||||||||||||||||

G. Choi is a Director of the Korea Fintech Society, Seoul, 02841, South Korea (e-mail: gpchoi88@outlook.com). Corresponding author: G. Choi. Received: September 10, 2022; Revised: October 15, 2022; Published: December 5, 2022.

|

||||||||||||||||||||||||||||||||||||||||

Despite potential benefits and strong interests in stablecoin, there are few that can deliver de facto stability, if not easing frictions among DeFi transactions. There is a trade-off between technical feasibility of reaching proposed stability and the governance issue of keeping it over time. Stability usually implies a peg with the dollar, but this falls short of stability for those seeking stable purchasing power. And most stablecoins are vulnerable to inflationary bias due to its peg to fiat money, while native tokens suffer from market crashes related with the recurrent lack of market liquidity. As such, seeking “stability” in crypto world is still a tougher challenge: Some seek a decentralized strategy (e.g., DAI), while others stick to centralized stablecoin (e.g., USDT, USDC). There are also algorithm-based stablecoins that carry innovative technique, but records show less than satisfactory performance over time [6][8]. It turns out that the stability enjoyed by the fiat currencies carries enormous economic costs as shown by attempts in the crypto world to emulate the nominal peg on denomination. That is, it requires tremendous efforts by non-sovereign issuers to achieve reduced volatility, especially over longer time horizon. Regardless of the composition of collateral pool and ways to engage in stabilization mechanism, however, reduced volatility still is the most desired feature in the crypto-driven DeFi arena. Based on the reality check that favors reduced volatility over a hard peg with the dollar, the primary focus on stablecoin development in this paper lies in introducing common features that promote the DeFi ecosystem. Therefore, given the rapidly expanding volume of literature on stablecoins, we first emphasize the design principle in the construction of stablecoin primarily for DeFi applications. |

||||||||||||||||||||||||||||||||||||||||

1.CoinMarketCap Top Stablecoin Tokens by Market Capitalization (as of March 10, 2022). |

||||||||||||||||||||||||||||||||||||||||

| II. LIQUIDITY IN DECENTRALIZED FINANCE | ||||||||||||||||||||||||||||||||||||||||

The primary goal of securing native token with reduced volatility is derived from the needs for market liquidity. Lack of liquidity restricts the potential of native protocol tokens to play a bigger role, and it can be overcome via repeated transactions among existing protocols. Therefore, reduced volatility per se is not a sufficient condition where liquidity concerns stay imperative within the ecosystem. In fact, the salient feature of generating liquidity in DeFi is different with the legacy system and the ground-up approach for networked liquidity is closely related with staking. This endogenous generation of liquidity is innovative as it hinges on AMM (Automatic Market Maker) and DEX (Decentralized Exchange). We first need to face the reality where there is no central bank that supply stable liquidity and there is no workable short-term money market The primary goal of securing native token with reduced volatility is derived from the needs for market liquidity. Lack of liquidity restricts the potential of native protocol tokens to play a bigger role, and it can be overcome via repeated transactions among existing protocols. Therefore, reduced volatility per se is not a sufficient condition where liquidity concerns are still imperative within the ecosystem. In fact, the salient feature of generating liquidity in DeFi is different with the legacy system and the ground-up approach for networked liquidity is closely related with staking. This endogenous generation of liquidity is innovative as it hinges on AMM (Automatic Market Maker) and DEX (Decentralized Exchange). We first need to face the reality where there is no central bank that supply stable liquidity and there is no workable short-term money market equivalent, and no deposit insurance facilities. Further, the most pressing issue within the DeFi ecosystem is the lack of pledge-able collateral, which requires pre-defined level of stability in value among assets that can be secured. Since liquidity is not provided by the centralized entity, it is important to generate it in a decentralized manner. In this setting, it is critically important to start building liquidity using stablecoin before strengthening various reward programs for longer-term staking, not vice versa. At the least, we need to secure pledgeable collateral for stable liquidity provision. Therefore, in the early stage of development, most have centered on reducing volatility, which still is the number one problem for DeFi expansion. Over time, we also have realized the need for resilience against shocks and efficient market transactions with less slippage. In short, reduced volatility, less slippage and stability remain the key design features for the DeFi expansion because these allow stable liquidity provision in a decentralized manner. |

||||||||||||||||||||||||||||||||||||||||

A. Incentives for Sustainable Liquidity |

||||||||||||||||||||||||||||||||||||||||

Specifically, the current project also emphasizes the role of stablecoin in delivering balanced incentive to various DeFi participants so that no excessive incentives are channeled into securing short-term liquidity with possible detrimental effect over the longer time horizon. Given the lack of term structure in DeFi, extra efforts to help ensure transactions in DeFi can be saved by designing stablecoins in the first place. We derive achievable stability by making use of available stablecoins and strengthen growth momentum by helping native token to generate extra market dynamics for the network, which will be channeled into a momentum for the seigniorage that supports the proposed stablecoin. The degree of dependency on existing stablecoin, i.e., fiatbacked stablecoin is decided by market acceptance of native protocol token for its feasibility. By separating growth dynamics from its inherent volatility, the protocol tokens can help generate extra thrust for the ecosystem expansion. For fragile startups, a stable funding source stays the key factor for any subsequent efforts. Typically, an ICO (Initial Coin Offering) type of fund-raising has experienced serious problems, e.g., pumping and dumping, carpet pulling, front-running, yet the next alternative STO still remains an incomplete option for projects. Even though one can resolve the short-term uncertainty using no action letters in major countries (e.g., South Korea), things are still murky and requires constant liquidity provision with no clear prospects for the future. In this vein, a hybrid stablecoin project seems a realistic approach to secure essentials for the community buildup and enhance transaction volume by offering incipient trust base for the ecosystem. |

||||||||||||||||||||||||||||||||||||||||

B. Governance for Liquidity Provision |

||||||||||||||||||||||||||||||||||||||||

| In addition to providing balanced incentives for liquidity, stablecoins also help with governance issues in DeFi to contribute toward enhanced interoperability. If there are conflicts within the ecosystem, the sustainability of the proposed stablecoin would be jeopardized. Therefore, given different interests among stakeholders, the choice of governance (e.g., DAO) needs to be further investigated for scalable decentralization. Reconciling conflicting interests in the ecosystem without sacrificing decentralization principles would require careful design as well as consistent stabilization exercises. It is this importance of background framework that often gets blurred since it exerts definite influence on the design of stablecoins for DeFi applications. Specifically, the incentives for LP staking are not a choice on its own, it should be part of the answers to solve the ecosystem liquidity problems of higher dimension. It is expected that relative weight of the fiat-backed collateral backing should remain below certain threshold even in cases that use the wrapped bitcoin (wBTC) as collateral. 4 This clearly reflects the implicit requirements of collateral for the DeFi application that primarily hinge on crypto assets for value exchange and delivery. Seiniorage needs to be strong enough for the community to consistently expand their ecosystem. DAO makes decision for the community interest. The automatic market maker protocol of decentralized exchange seizes liquidity for each pair of cryptoes, but incentives to lock up liquidity varies. By allowing exchanges for market liquidity, the enablers are enjoying excessive profit, and this is often dubbed as liquidity farming. This practice also reminds us of the Ponzi game. The tokenomics in DeFi do not add to producing strong incentives for the successful completion of the proposed project. Rather, it diverts attention toward investors such that major decisions for the project are skewed toward speculation, including specific airdrops. The simple reason for this is the lopsided difficulty of running the project to produce any concrete results as compared with liquidity provision to keep the project running. What is this contradictory move that plagues the minds of our core developers in the de facto money game? This practice of tokenomics reminds us of the difficulties in promoting a decentralized ecosystem from the scratch. Providing extra return to Oracle would help us solve liquidity problems in layer 2 network. While order books are commonly known from traditional and centralized finance, the DeFi space has brought about another innovation: pooled liquidity and automated market making. For example, on Uniswap, investors exchange one token for another trade against a pool of tokens. The price is not defined by a bid-offer spread, but instead by the composition of the pool (called the “constant product market maker model”). Similarly, money markets such as Compound allow lending to and borrowing from a pool of tokens, and the interest rates are set algorithmically depending on the degree of pool utilization. In this context, the governance is still the pivotal issue for ecosystem build-up. In filling up the gap that is generated from a move from the centralized paradigm, it is important to keep balance lest we tend to seek some corner solutions of decentralization. There are also key parameters in keeping the ecosystem stable, helping TOK stays within the bound of weak form of Dollar pegging. Unlike DAI, however, the collateral ratio can be kept at below 100% since there is stablecoin to reduce the burden of stabilization. |

||||||||||||||||||||||||||||||||||||||||

4.The relative weight of legacy assets and stablecoin is determined by parameters regarding composition of collateral as well as stabilization needs by the off-chain oracle feed. |

||||||||||||||||||||||||||||||||||||||||

C. DeFi Stablecoin as Balanced Reward Incentives |

||||||||||||||||||||||||||||||||||||||||

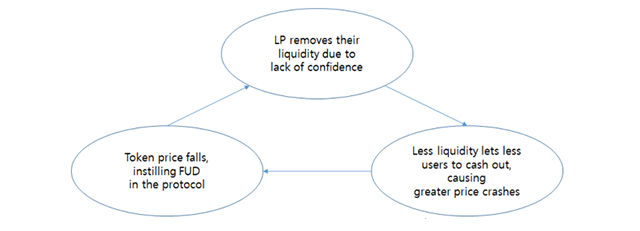

| Among the key elements that interfere with market liquidity provision are incentive structure and governance, which dictates the price of native tokens over time. And there is a tradeoff between token price and liquidity provision since liquidity is secured mostly via staking in the ecosystem. The increased liquidity is only possible by offering greater benefits to existing token holders, especially in the short run. Consequently, the unifying theme for this effort is to allow stablecoin to kick start the growth momentum in the DeFi to move toward a better equilibrium when basic market infrastructure still is fragile. There exists very narrow window for first liquidity to generate extra return over time, which will support token price over the longer run. If this fails, the token issuer will be under greater pressure to offer increasing returns to secure minimum level of liquidity. This means usual tokenomics of stablecoin need to embrace the bigger picture to remain relevant incentives for growth and stability. In short, the requirement for managing liquidity interferes with native token price over time and increasingly sizable resources need to be diverted to raising liquidity via strengthen incentives, distorting stakeholder interests in increasingly complex governance. So, the overall breakdown of the support partly comes from existing stablecoins, which offer basic minimum stability that holds the volatility of crypto within a certain bound. And this derived stability stays a fragile support when endogenous momentum for seigniorage cannot be secured. In other words, the proposed ecosystem hinges on the workings of hybrid stablecoin at the center of exchange for liquidity and value creation. As such, unlike traditional finance, with unpleasant implications for unlimited printing, the newly emerging alternative finance on blockchain has an inherent stabilization mechanism in place. If the balance is lost somewhere, the whole ecosystem faces systemic risk, and the internal mechanism and protocols prohibit excessive risk-taking in advance. Instead of finding sources of trouble in a specific location that brings about an on/off solution without system upgrade, the DeFi approach allows us to consider the whole ecosystem and its inner workings to improve scalability without sacrificing stability. In short, the connected collateral framework forces the necessary adjustments before it threatens the overall stability. This is the main feature of the DeFi system that supplies better liquidity provision than other alternatives. In contrast, credibility supported by a group of elites in the legacy world has proven less effective as a system for allocating resources efficiently. Rather, this new paradigm based on blockchain, despite its negative impact on traditional finance, surely delivers better promises, because its core message touches on meeting the challenges in a highly connected world. Given the DeFi stacks on different blockchain, the direction for change becomes obvious in that more interoperability needs to be secured, otherwise the current practice in a siloed manner would face serious challenges. And we need a type of linker in the form of stablecoin to help connect with various blockchains. To address issues related with securing liquidity in DeFi, a new breed of collateral has been tried, e.g., reserves of legacy assets, crypto and physical assets [6]. However, these imported pillars for trust cannot function properly in DeFi due to its inherent centralized characteristics and legacy stakeholders. Maker DAO has tried the first innovative approach using a truly decentralized stablecoin Dai protocol. However, the promised stability has been challenged often so it includes USDC to shore up the dollar peg. As shown by DAO, true decentralization proved hard to implement even in native blockchain setting. Given the stalemate situation, the DeFi protocols are trying to take care of its liquidity problem by incentivizing staking among existing crypto holders by offering extra return for longer and bigger staking in liquidity pool. By locking up their crypto investment, the holders can enjoy much higher return than what legacy worlds use to offer. However, this creates problems that cannot be detected until it becomes impossible to manage, i.e., creating vicious cycle of vetting investments for higher return down the closed chain run by individual DAOs. In fact, “negative flywheel effect (see Figure 1)” that constantly requires ever-increasing commitment of resources to secure liquidity could backfire to amplify the negative feedback loop when there is a regime change toward higher interest rate environment in legacy world. The so-called liquidity mining via native token emissions cannot function properly in the deleveraging period and extra stabilizing strategy, e.g., delta neutral staking, needs to be applied. Even for these time consistent strategies to be applicable, stablecoin needs to be introduced and implemented before situations get worse. |

||||||||||||||||||||||||||||||||||||||||

Source: https://docs.olympusdao.finance/pro Fig. 2. Loss and gain regions of three AMMs |

||||||||||||||||||||||||||||||||||||||||

| There are also issues of competing reward programs in DeFi without addressing underlying problems related with vulnerable collateral base. In June 2021, providing liquidity on Compound was further incentivized through the distribution of their governance token, COMP. As a result, there are two ways coin holders are compensated: one is the return from staking and the other is from the governance contribution to a new platform. This also had the effect that both borrowing and lending became profitable, since COMP rewards are more valuable than the interest paid. Sometimes, the latter is more important than the former. Along the success of Compound’s token, other parts of the DeFi ecosystem have also started to incentivize liquidity through platform governance tokens. Balancer, a decentralized index fund creation protocol with automated index rebalancing, started handing out BAL tokens to platform participants. Similarly, pools of various forms of tokenized Bitcoin on Ethereum, such as wBTC, sBTC and renBTC can earn various governance tokens associated with the involved protocols. Therefore, incentive structure and/or governance setting on its own cannot provide stable liquidity over time since the endogenous liquidity generated by market transactions can only be secured via hybrid stablecoin in the initial stage for DeFi ecosystem. | ||||||||||||||||||||||||||||||||||||||||

III. DESIGN PRINCIPLE AND MECHANICS OF DEFI STABLECOIN, TOK 5 |

||||||||||||||||||||||||||||||||||||||||

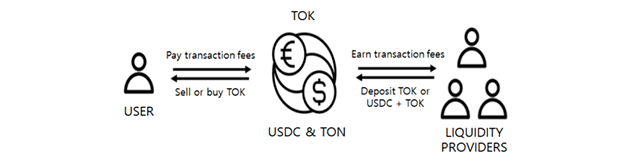

| Based on previous discussions, we can thus lay out the design principle for DeFi stablecoin: First, DeFi needs to build up market trust by utilizing legacy trust in a dynamic setting. Instead of paying extra costs involved with volatile assets, it is necessary to moderate volatility before engaging in transactions. In practice, greater APY in DeFi often comprises cost factors for dealing with volatile and less liquid assets. Second, transactions in the ecosystem should remain frictionless. Sizable traffic among on-chains involves significant gas fees and delays related with congestion. Even with layer-2 options, it is better to prepare for frictionless transactions in the ecosystem. Third, market needs for swapping, lending, and borrowing are channeled to generate commerce driven transactions. This is often in conflict with the prevailing cases where transactions are made primarily for staking and yield farming. If there are enough market tractions, TOK will grow to be a commerce-backed stablecoin on its own. By comparison, the reason the USDC is stable is due to its trade volume. The only way to achieve true stability is through building trade volumes by identifying market needs, including possible cross-layer transactions. Similarly, the viability of stablecoins critically hinges on its use on a grand scale, which requires dynamic interactions on chain, including the newly emerging NFTs. 5.https://medium.com/onther-tech/tonstarter-phase-3-starter-guide-en-kr-ab97bb9e50fc Specifically, the proposed design agenda for initially reducing volatility should contribute toward promoting “flywheel effect of virtuous cycle” where individual actions add to overall incentives for the ecosystem build-up. This can be achieved by locking up native protocol token with that of a stablecoin instead of trying with native protocol token only that needs extensive and constant adjustments. Further, there is a real risk “stablecoins” would be anything but stable without robust legal and economic frameworks, which implies that some legacy backing on stablecoin is necessary to start building market confidence in a new field. In fact, earlier episodes of market turmoil demonstrate the vulnerability of stablecoins as seen by the cases where the movements frequently exceed the pre-defined upper/lower boundaries. To overcome this problem, the proposed solution encompasses all the necessary stabilizing resources available, which include the hybrid nature of underlying collateral reserves. We also expect that there should be comprehensive regulatory structure in place soon. This paper tries to answer specific needs of the DeFi community with native tokens by offering realistic approaches that should remain time consistent. In one way or the other, the overall comparison of various protocols available today clearly confirms the common denominator of reduced volatility for stablecoins to remain relevant in a broader context. For proposed stablecoin to serve the needs for ecosystem expansion via seamless market transactions in DeFi, we also gather the following: the implications from the literature review [7] point toward the direction for full recognition of regulatory environment, initial conditions, and actual market practices in DeFi. In addition to reducing volatility, we need to recognize how we achieve this in the context of incentive schemes within the community. In fact, the current tokenomics often emphasize community-based reward program that often come into conflict with earlier incentives as well as other community native tokens. The conflicted incentive structure that underpins underlying volatility needs to be streamlined with the use of stablecoin for maximum network effect, e.g., vehicle currency in real world applications. And the proposed stablecoin is seen as the ultimate tokenomics with built-in incentives for the ecosystem. In short, we try to deliver products that suit the needs of diverse group of market participants, including investors, arbitrageurs. It is undeniable that diverse groups of stakeholders in DeFi have different time horizon and risk appetites, and the short-term reward programs often come into conflict with those of longer-term investors since dynamic equilibrium is poorly defined. Therefore, we look to design stablecoin not only targeting specific level of volatility associated with deep parameters, but also recognizing overall incentive schemes associated with a particular stablecoin setup. This would allow the proposed stablecoin to keep balance in market liquidity in a dynamic setting. Against the backdrop, we employ the Tokamak network to experiment the proposed stablecoin, which we dub as TOK, which has a unique advantage as a balanced protocol token on Ethereum. It exemplifies as one of the candidates for commerce in the ecosystem. In addition to satisfying requirements for generating liquidity, the proposed stablecoin corrects incentive scheme toward a more balanced one such that all stakeholders enjoy balanced benefits over time. DeFi stablecoin can help formulate many links for diverse interactions in this highly connected environment. In fact, the layer-2 Tokamak network allows us to exploit scalability without sacrificing decentralization and the combinatorial management of collateral resources would further enhance stability under different settings. Up until recently, however, very few stablecoins satisfy all the necessary requirements, prompting these existing centralized stablecoins continue to play a pivotal role in the DeFi ecosystem as de facto collateral6 . In short, we employ methods to reduce volatility with the proviso that the hybrid structure still is consistent with the overall incentive structure and governance constraints for longer-term ecosystem expansion via increased interoperability. The critical vehicle for this to happen is to use DeFi stablecoin that dynamically relies on relative prices of collateral and protocol token as well as market conditions and overall risk appetites of various stakeholders. Accordingly, the proposed DeFi stablecoin system consists of two stacks: One is the collateral pool and its dynamic index, and the other is the tracking mechanism to keep the target variable within a pre-specified band. 6 In Holmström and Tirole [15], assets with the property that the cash flows are “pledgeable” provide insurance against possible adverse events in which agents need “liquid” instruments. Given the lack of workable alternative for crypto participants to produce safe assets in the first place, the only option available is to borrow trust from the legacy world in proportion with its prevailing capacity to secure trust. The former is an index of collateral, and the latter is the discretion in its decision to stabilize the target over a specified time interval. Our unique proposition within this landscape lies in our tailored collateral of hybrid assets. For the cryptocurrency ecosystem to expand, it needs to be able to offer an option for various users with various risk appetites. The collateral composition maps the risk appetite and user preference into a set of collateral whose relative weights can be adjusted. What we aim to show is a combination of TON, a tokamak native token, and other stablecoin assets. Depending on the user’s risk appetite they can choose how much TON they would like to include in their collateral, which also relies on its current price as compared with its equilibrium price7 . The changes in the price of native token gets fed into the index in terms of its deviation from its MA (moving average) or simply its HP (Hodrick-Prescott) filtered value. In fact, this strategy can be applied to other cryptos in the future, yet Tokamak network is one of the few networks with all the features necessary to complete the virtuous cycle in the crypto ecosystem. Considering that TOK has significant upward potential from its TON starter program, there will be a market and a real demand for TOK. Our TOK is not a strict form of stablecoin because we can allow some room for price fluctuation over time. Effectively, TOK reduces volatility as it supplies downward protection against various shocks. This flexibility with upward potential and downward protection is a unique feature to overcome the heavy regulatory oversight [18] that increasingly emphasize the use of legacy reserves with deposit insurance as the only legitimate collateral. By design, TOK is a hybrid, composite stablecoin with half dynamics from its own commerce and the other half from existing stablecoin platforms. The relative weights in the dual structure come from relative volatilities of basket weights. And the Tokamak DeFi ecosystem will develop into a full-fledged decentralized finance hub that connects all the primary DeFi use-cases within the open and collaborative ecosystem. In short, the benefits of DeFi should be easily accessible to the masses but in a secure and intuitive way, avoiding the expensive fees, confusing interfaces, and centralized decision-making of current platforms. Specifically, given the high volatility of native token, around 70~90% of the value of TOK will be collateralized initially by USDC or equivalents. That means that in the absolute worst case, a TOK holder could never lose more than 10~30% of their invested capital. Expectedly, for those with strong risk appetite, there is little incentives for stablecoins in the first place. The remaining 10~30% of TOK’s collateral value is where the commerce element comes in because it will be backed by our TON or other extended applications within or across the platforms. As the TON appreciates via increased adoption, the proportion of TON in TOK would increase and TOK and TON can be merged eventually. For now, users use their stablecoins to generate better return in a different manner. Here they are not restricted in the use of their stablecoin to earn more return. They can always get back their original investment whenever they want. The extra return from their investment comes from better utilizing available resources as well as network externality. The issue of this hybrid coin also benefits from increased liquidity as well as resources for staking and other investment opportunities (see Figure 2). Using existing stablecoin other than DAI allows us to save on overcollateralization requirement of Maker DAO. Also note that unlike algorithmic stablecoins, there is no minting/burning of TON within the stablecoin itself, removing potential minting vulnerabilities that have been exploited in other protocols in the past. |

||||||||||||||||||||||||||||||||||||||||

Fig. 2. Process of TSWAP |

||||||||||||||||||||||||||||||||||||||||

7 Given the lack of theoretical foundations for TON, a practical approach presumes the moving average or HP filtered value as equilibrium so that deviation from it dictates future dynamics. |

||||||||||||||||||||||||||||||||||||||||

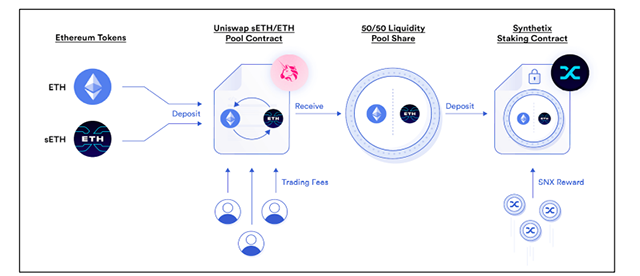

| Rather, Tokamak stablecoin TOK is an autonomous one that reflects relative price changes and risk appetite over time, with minting and burning operation when the actual price deviates from the pre-agreed band. To be fair though, you could say that TON, like most crypto tokens, are volatile, and would not be accepted as collateral in a protocol like MakerDAO. Yet, TON are much more resilient to market pressure than new governance tokens for LP rewards thanks to the following stability mechanisms TOK will have. By allowing TON onboard with Uniswap directly via TOK, we can utilize the feature of CFMM that provides incentive to correctly report the price of an asset, and the decentralized exchange can serve as a good on-chain price oracle that other smart contracts can query as a source of truth (see Figure 3). The benefits of utilizing stablecoin are much broader than a simple saving related with reduced volatility | ||||||||||||||||||||||||||||||||||||||||

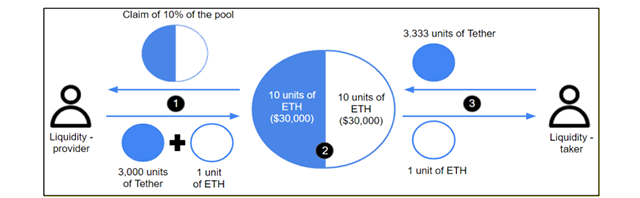

Note: Initially, we assume 1 Tether = $1, 1 ETH = $3,000 and for a pair of 27,000 units of Tether, and 9 units of ETH, each worth $27,000. Source: [1]. Fig. 3. DEX and CPFM (constant production function market maker) in DeFi. |

||||||||||||||||||||||||||||||||||||||||

Against the possible burden associated with TON linkage, stability fee may be necessary for redeeming TOK. However, part of legacy stablecoin can help minimize costs and extra return from TOK for yieldfarming can generate extra return compared with cases where one holds on to centralized stablecoin or TON single-handedly. Unlike the DAI protocol, the extra savings from holding existing stablecoin can be greater than the needs for extra return from holding decentralized stablecoin because extra costs incurred in stabilizing the latter one. Also, one can save the equivalent of Dai Savings Rate (DSR), because the possible interest rate earned by holding TOK (i.e., staking reward) over time is almost automatic, lessening the incentive burden to increase the demand for TOK, which has built-in upward pressure from the TON ecosystem. Overall, the cost reduction comes from targeting a stable collateral mix and the interventions by the Treasury are considered automatic using the smart contracts. As such, the open dynamic reserve structure and the transparent engagement principle remain the backbone of the TOK stablecoin. In this vein, the newly introduced stablecoin based on Tokamak Network brings together new innovations in collateral composition and stability mechanism to ensure tailored stability features that tend to differ among diverse groups of investors. The reliance on numerous factors for securing liquidity differs from the traditional liquidity mechanism based on interactions of inside and outside liquidity with public and private suppliers as explained by Holstrom and Tirole [15][16]. Given the overriding importance of securing on-chain DeFi liquidity, we can sum up the design principle of DeFi stablecoin such that some of the identifiable prohibitive factors need to be controlled before engaging in liquidity generation. That is, given the fragile condition of the incipient Tokamak network, its inherent volatility needs some moderation to engage in more efficient transactions for liquidity. As explained, the stablecoin protocol matters since its viability depends heavily on its choice that decides collateral mix, stabilization mechanism, and overall incentive schemes in a dynamic setting. |

||||||||||||||||||||||||||||||||||||||||

A. Stable Collateral Pool Index |

||||||||||||||||||||||||||||||||||||||||

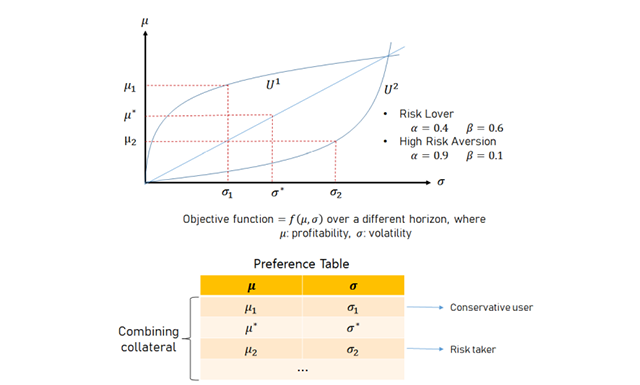

| Since there are an entire range of risk appetites among investors and other participants over different time horizon, the definition of stability can be further differentiated. We can approximate target price movement that corresponds to , which will be tracked by . That is, the dynamic price index around a predefined dollar peg consists of global stablecoin and native protocol coin with key parameters of and theratio of and the deviation of protocol coin from its long-term equilibrium (see Figure 4)8 . | ||||||||||||||||||||||||||||||||||||||||

Fig. 4. Risk preference map for the choice of parameters in the dynamic index |

||||||||||||||||||||||||||||||||||||||||

| Given the risk appetites, collateral combination is determined, and the dynamic index is maintained. This entails complicated operations as TOK can be further tailored, but it all depends on the budget and Treasury capacity. Even among the TOK family, collateral composition for a particular TOKi can vary, but here we just emphasize the possible configurations for specific category of investors. From the operation perspective, the first step is to construct a dynamic index of eligible collateral for the proposed stablecoin that is pegged to the US dollar. Here we call the stablecoin price index as the combination of global stablecoin and native crypto token such that: |

||||||||||||||||||||||||||||||||||||||||

| where is the price of the TOK hybrid DeFi stablecoin, is the price of global stablecoin, is the price of the filtered value (moving average of 60 days or HP filter with optimal weights), and is the value of TON (or native protocol token). This can be redefined and expandable to include other stablecoin or legacy assets, and NFTs. If this index represents the price of a dollar or value of stablecoin, then the proposed DeFi stablecoin TOK is a combination of eligible collaterals. The hybrid mix ratio α can be determined endogenously or exogenously depending on situations. The value α determines relative contributions of both legacy and crypto component depending on the relative prices of component collateral and risk appetite. There are two distinct mechanisms in play, the first one is backing stablecoin with fiat assets to qualify as asset-linked stablecoin, and the latter see to use algorithms to change the supply of stablecoin in response to changes in demand. Due to its dual features, the current attempt is called hybrid stablecoin. In fact, the TOK utilizes all the available features to seek stability and allow growth via increased network effect. Therefore, it can be extended to include multi-collateral if the proper Oracle services become available. The synthetic nature of collateral index can be expected in the presence of a newly recognized financial arena, e.g., metaverse and NFTs. This just illustrates that price stability or controlled volatility can only be achieved in the ever-expanding world by incorporating a new breed of assets in the collateral pool in an index form so that market interventions can be applied in times of crisis. 8 are relative weights of the dynamic price index for a proposed stablecoin, where utility function U is determined by expected return and volatility with a scaling factor k and the coefficient of risk aversion such that . For a given reflects risk averseness, while depicts risk lover’s choice for volatility. Preference table shows various combination of for a given risk appetite to determine the collateral mix, and the acceptable level of volatility for a given expected return . 9 Reference or anchor global stablecoin with a full collateral backup, e.g., USDC or some alternative composite index. |

||||||||||||||||||||||||||||||||||||||||

B. Stability Mechanism |

||||||||||||||||||||||||||||||||||||||||

| As shown, the dynamic index of collateral consists of pillar stablecoin and eligible protocol tokens that need stabilization. Building on the dynamic index, which is a collateral pool that maps the value of target variable pegged stablecoin over time. It is our goal to keep it within a pre-specified band so that holders of stablecoin have no need to engage in transactions for arbitrage. For this, we can apply the stability mechanism if necessary. Specifically, the proposed stablecoin hinges on two-tier stabilization mechanism: One is the collateralized index that takes care of volatility to a specific extent by incorporating the existing stablecoin. The other mechanism is Treasury initiated market intervention that helps price movements within a specific band. Here we rely on CDP (Collateralized Debt Position) of MakerDAO Mechanism as target indicator. Further, we can exploit the stabilization mechanism of the Terra-Luna system that triggers specific actions if the target deviates from the specified band. To solve for possible collateral pool, there have been attempts ranging from physical assets, legacy instruments, and purely crypto assets. The other variable to solve is diversifying collateral types. The construction described above does not just work for long BTC spot, short BTC-USD perp. In theory, UXD Protocol is compatible with any (trust-minimized) collateral. Contract support for a diverse set of collateral types makes UXD more scalable. UXD can also extend to support other stablecoins including EUR, YEN so long as there are liquid futures contracts denominated in that currency (e.g., BTC-EUR perps or futures). The novelty of our approach is its hybrid composition of collateral as well as varying weights of governance coin where its importance decreases with its price decline, vice versa. Overall, we maintain the constant value of the collateral pool by adjusting its composition depending on its price changes over a specified time interval. This dynamic collateral pool is equivalent with our proposed stablecoin. It is simply a time-varying index of the collateral pool over time. In this paper, we mostly confine our attention to constructing dynamic index and Treasury functions10 . |

||||||||||||||||||||||||||||||||||||||||

| Stability Mechanism 1 — Dynamic Index and the Treasury | ||||||||||||||||||||||||||||||||||||||||

| In tracking the dynamic index of hybrid collateral, we can expect trading between the index and the component and trading fees from TSWAP will go towards the treasury. However, this portion will be flexible in scenarios where the peg is below or above $1 to reinforce the peg. Due to this cost, a small fluctuation would not result in active trading, while a move outside the band would trigger equilibrating transactions. And a small amount of redemption fee will be charged on each TOK to support operating costs. A portion of idle treasury will be deployed within strategies on safe external protocols to earn yields to feed back to the treasury, growing it over time. If the treasury is full and can cover pre-specified proportion of the outstanding market cap of TOK, then TOK will always be fully collateralized, and arbitrageurs and traders will always keep the soft peg. Benefits of holding a security token is that one has the right to claim dividends and make decisions on the revenue generated by the token issuer, distribute assets in small units, as well as convenience in trading assets cross-border. Unlike utility tokens that ICO has tried to prove that they are not securities, securities tokens are self-proclaimed tokens that comply with SEC securities regulations. And the security tokens can overcome issues related with government bonds that carry a lengthy process involving multiple intermediaries and a complicated method of taxation that is ridden with human error, which have constrained the cross-border usage as collateral. In fact, security token has enormous potential to change the dynamics of capital markets. 10 As a modeling exercise, stability mechanism using dynamic index is extensively investigated in this paper, while other mechanisms will be actively involved later |

||||||||||||||||||||||||||||||||||||||||

| In fact, security tokens have potential to democratize the way financial services are delivered. The following are usual practices to solidify internal resources to improve the protocol positions in the market. Or we can directly maintain dynamic mix of eligible collateral to support the pre-specified peg and the Treasury intervenes only when the movement exceeds the pre-defined band. This operation can be further automated via extended smart contracts that controls liquidity incentivization (see Figure 5). |

||||||||||||||||||||||||||||||||||||||||

| Stability Mechanism 2— TOK Staking Support | ||||||||||||||||||||||||||||||||||||||||

| As we grow TOK’s utility, it will have potentially trading pairs and connected farming pools. However, to start with, we will have TOK-USDC. This pair will receive a considerable number of TON emissions to incentivize early holders of TOK. In time, these emissions will spread over other pairs. In addition, the emissions rate itself will serve as a stability mechanism for TOK’s soft peg. For instance, every .001 that the TOK peg drops under $1 on a 24-hour TSWAP, allocated emissions for TOK can be adjusted down. Vice versa, for every .001 that the TOK peg is above $1 on a 24-hour TSWAP, we will increase allocated emissions for TOK by a pre-specified. | ||||||||||||||||||||||||||||||||||||||||

Source: https://blog.chain.link/defi-2-0-and-liquidity-incentivization/ Fig. 5. Smart contract for liquidity incentivization. |

||||||||||||||||||||||||||||||||||||||||

| Stability Mechanism 3— Emissions Support + Bonding Incentive | ||||||||||||||||||||||||||||||||||||||||

| Like other DEXes, TON emissions acting as rewards for LPs are one of the building blocks of the AMM model, providing the incentives for LPs to stake, which in turn creates sufficient liquidity for traders to use the exchange. However, to keep APYs high for LPs, TON prices need to stay high. This requires extra activities. For this, TOK doing buybacks of TON to hold as 10% (adjustable) of its collateral and locking those tokens up will create significant buying pressure on TON, so that APY for LP farmers on TVault will increase. Furthermore, the DEX activities should add significant volume and trading fees. Therefore, it makes sense that TOK and TSWAP will have a codependent relationship that builds a positive cycle of reinforcement. Potential resources are accumulated in the Treasury, making sure it is ready to deploy in times of market turbulence. In a related context, vetting practices can also disrupt the level-playing field. The initial coin distribution can inadvertently create problems for subsequent allocation since the decision can be highly skewed in favor of initial investors and stakeholders. By restricting the entry for liquidity provision, especially by creating the hurdle rate, the payoffs for the incumbents can be exaggerated. This practice can be indirectly mitigated via the use of stablecoin since the accompanying incentive scheme can be more balanced than the case of native tokens. |

||||||||||||||||||||||||||||||||||||||||

| Stabilization Mechanism 4 — Insurance and Cross-chain Extension of Layer 2 | ||||||||||||||||||||||||||||||||||||||||

| We can also utilize other extensions and interactions to help secure and benefit from the price stability of TOK. In fact, the need for insurance services in DeFi seems enormous as reported in Chainlink [4]. In 2021, the price of the DAI was driven up 30% over its $1 peg, which was used as the pricing oracle by the Compound DeFi credit platform, it caused Compound’s smart contracts to determine that many loans were under-collateralized. This triggered massive assets to be liquidated automatically. In fact, related events took place, penalizing early participants in DeFi, and some compensatory efforts to earlier investors become unavoidable. Unlike fiat currencies, crypto tokens suffer from the extra needs to manage incentive schemes over time, which is destabilizing. This event illustrated the vulnerability in the interconnection among DeFi and other blockchain-based financial systems. And the current expansion of DeFi space can erode competitiveness across chains since incumbents will formulate closed markets among themselves, e.g., Curve by forming alliance that restricts or favors the LP to a pre-defined pool. In most cases, joining in the specific liquidity pool requires stablecoin status in the first place. Lack of this requirements can lead to the erosion of competitive environment and frictions in the ecosystem. In this context, insurance smart contracts use input oracles to verify the occurrence of insurable events during claims processing. Output oracles can also provide insurance smart contracts to make payouts on claims using other blockchains or traditional payment networks. Since stablecoins are a critical part of DeFi because they provide collateral and low-volatility payments, reliable oracle services which developers can quickly integrate into their dApps become available only when stablecoin is ready. Sharing the common property of stablecoin in the DeFi ecosystem, the overall network effect can be sizable. Enterprise systems can read/write to any blockchain and perform complex logic on how to deploy assets and data across chains and with counterparties using the same oracle network. The result is institutions being able to quickly join blockchains in high demand by their counterparties and swiftly create support for smart contract services wanted by their users without having to spend time and development resources integrating with each individual blockchain. |

||||||||||||||||||||||||||||||||||||||||

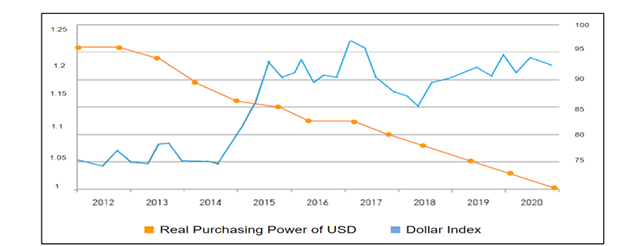

Note: Real Purchasing Power of USD pertains to the left vertical axis. Dollar Index pertains to the right vertical axis. Fig. 6. De facto stability over different time horizon |

||||||||||||||||||||||||||||||||||||||||

Stabilization Mechanism 5 — Perpetual Derivatives Exchange |

||||||||||||||||||||||||||||||||||||||||

| In a different setting, we can use derivatives market to enhance stability. This can be explored if the current and future regulatory environment makes the approach untenable over time. In this context, each TOK token (different version of TOK that does not use stablecoin as collateral) can also be backed by a delta-neutral position on a perpetual derivatives exchange when situations mature. Users deposit collateral such as TON to the protocol and receive $1 of TOK in return for every $1 of TON deposited. The TON is then deposited to a perpetual exchange protocol as collateral and then an opposite short position is taken at the same value of the deposited TON. So, if the price of TON falls -10%, the deposited TON collateral would lose -10% of USD value, however, at the same time, the short position would gain +10% of USD value resulting in a net 0% move of TOK’s collateral in USD terms. Having a net 0% move on the underlying asset is the definition of delta neutral. Effectively, the TOK protocol simulates having stable assets as collateral but with volatile assets enabling it to back each TOK token 1:1 with decentralized assets. When a user wishes to redeem TOK for collateral, the process flows in reverse. Users burn TOK with the protocol and in return receive the exact USD amount in TON or the collateral token of their choice. To return the user’s TON, the protocol closes the TON short position on the perpetual exchange for the exact dollar amount of TOK burned and the freed-up TON collateral is withdrawn to the TOK protocol at which point it is returned to the user. |

||||||||||||||||||||||||||||||||||||||||

IV. EX-POST CHECK ON TOK STABLECOIN |

||||||||||||||||||||||||||||||||||||||||

A. Stability of Purchasing Power |

||||||||||||||||||||||||||||||||||||||||

| We have observed that even the predominant vehicle currency has shown gradual erosion of its purchasing power over time (Figure 6). And this aspect needs recognition in the construction of stablecoin index that searches for a degree of pegging with the US dollar. Stability as a store of value is not the desired feature in the crypto world, yet. However, the design of money as illustrated by money flower [3] needs pre-defined goals and revealed preferences. Pegging the dollar index would supply the maximum stability, yet its dynamic stability gets constantly sacrificed over time. Extra liquidity provided by the seigniorage of fiat money stays the backdrop for us to seek alternatives for the storage of value. This also reminds us of the self-imposed restraint for exploiting the power of crypto seiniorage as LP staking reward. | ||||||||||||||||||||||||||||||||||||||||

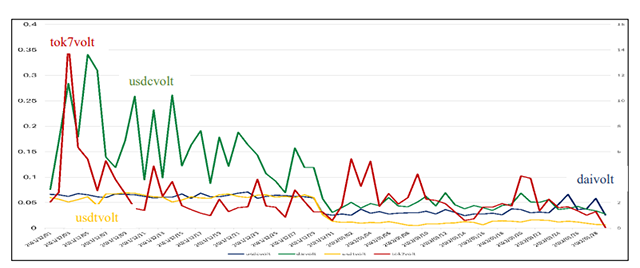

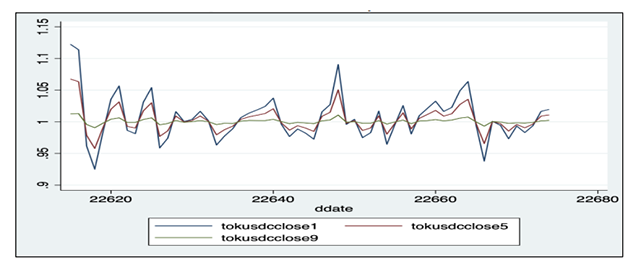

Note: Left Vertical Axis–USDC, DAI, USDT • Right Vertical Axis – TON. Data Source: CoinMarketCap API Fig. 7. Volatility comparison (usdcvolt, daivolt, usdtvolt and tok7volt |

||||||||||||||||||||||||||||||||||||||||

| B. Volatility as Shown by Reduced Volatility | ||||||||||||||||||||||||||||||||||||||||

| There are several factors impacting the volatility performance over time (Figure 7). However, we can easily observe reduced volatility when the mix of native crypto gets combined with the fiat or stablecoins. Also, as expected, heavier reliance on stablecoin also yields better reduction in stability regardless of the frequency window. The graphs of the stablecoin TOK by α are as follows (Figures 8, 9, and 10). |

||||||||||||||||||||||||||||||||||||||||

| C. Slippage (Impermanent Loss) | ||||||||||||||||||||||||||||||||||||||||

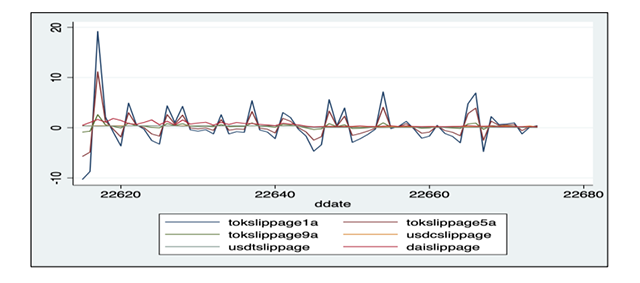

| The measurement of slippage is a complicated task, yet we can proxy this using the gap between opening and closing price. As predicted, we can confirm the slippage reduction by using stablecoins as trading pairs. Higher correlation allows less slippage in constant market maker models. The preliminary results confirm that stablecoin TOK based paring is a better choice for LP and other leveraged transactions in DeFi (see Figures 11 and 12). | ||||||||||||||||||||||||||||||||||||||||

Note: Comparison of TON, USDC, and TOK Fig. 8. Ex-post check on the feasibility of TOK stablecoin. |

||||||||||||||||||||||||||||||||||||||||

Note: Configurations of TOK stablecoin using USDC as an anchor and adjusted weights of the native token TON. Data: CoinMarketcap API. Fig. 9. Different configuration of TOK stablecoin by . |

||||||||||||||||||||||||||||||||||||||||

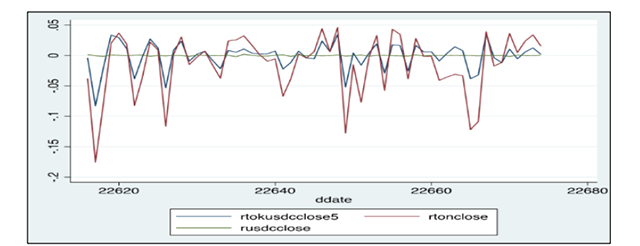

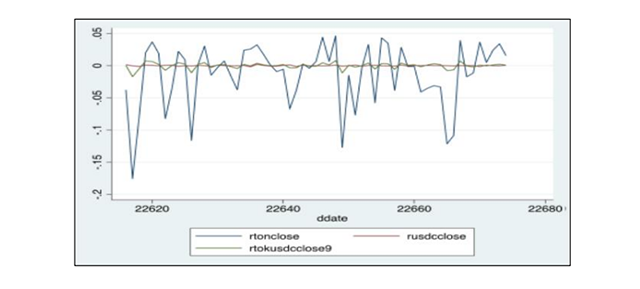

Note: rtokusdcclose5 is a TOK stablecoin α with =0.5, rusdcclose, rtonclose represent returns of USDC, and TON, based on closing price, respectively. Fig. 10. Comparison of returns volatility among different crypto assets by ‘’. |

||||||||||||||||||||||||||||||||||||||||

| D. Dynamic Stability (Second Moment) | ||||||||||||||||||||||||||||||||||||||||

| Among major frictions we can easily observe in the DeFi protocols, the feature of dynamic stability stands out. This is because of the complicated nature of preserving liquidity using collateral as backups. Regardless of the situation, it is important to remain robust by holding on to safe assets or HQLA (High Quality Liquid Assets) status of collateral. Even with similar pattern of shock responses, the vertical axis represents the differences in magnitude against shocks. Here we examine and compare responses of the collateral pool against various shocks (see Figure 13). We expect a robust performance of hybrid collateral pool against serious shocks, irrespective of time horizon (e.g., y-scale). | ||||||||||||||||||||||||||||||||||||||||

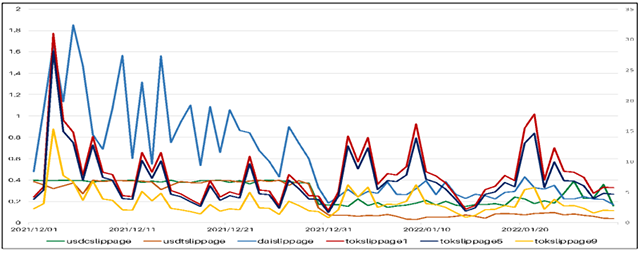

Note: Left Vertical Axis–USDC, DAI, USDT • Right Vertical Axis–IRON, FRAX, TON Data Source: CoinMarketCap API. Fig. 11. Slippage comparison. |

||||||||||||||||||||||||||||||||||||||||

Fig. 12. Comparison of TOK slippage by ‘alpha.’ |

||||||||||||||||||||||||||||||||||||||||

| E. Eligibility Measure of Stablecoin | ||||||||||||||||||||||||||||||||||||||||

| Here we examine and compare the distance to No Questions Asked, which is inversely related with the convenience yield of stablecoin. As shown in Figure 14, Black-Scholes formula has been modified to calculate the value of put-option of various stablecoins, and the TOK stablecoin looks relevant compared with DAI. Stablecoins can be interpreted as non-interest- bearing perpetual debt with embedded put options for redemptions at par on demand from the issuer [12][17]. Reduced volatility, less slippage in DEX transactions, balanced incentives over time, stronger robustness against shocks, and continued throughputs from communitybased commerce are among the notable requirements for DeFi stablecoins. The changes in the right direction have been made possible by including some level of legacy collateral input. Given the limited traction in the ecosystem for eligible collateral, the legacy component of trust cannot be ruled out in devising the DeFi stablecoin. The above criteria for stablecoin remain the guiding principle for future design and implementation going forward. And it is important to improve the interoperability across various blockchains by embedding the features of stablecoin at the outset before expecting rich dynamics within the DeFi ecosystem. | ||||||||||||||||||||||||||||||||||||||||

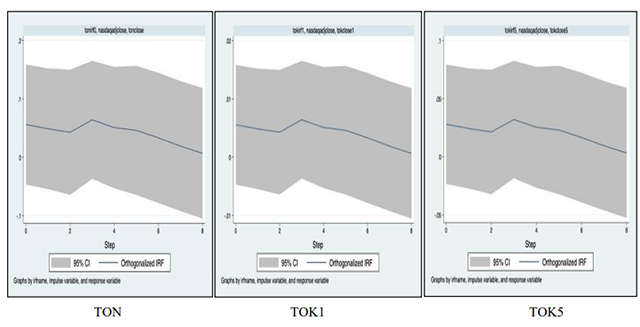

Note: TOK1 (a=.9), TOK5 (a=.5). Patterns look similar but y-axis show different magnitudes. Fig. 13. Dynamic shock response functions. |

||||||||||||||||||||||||||||||||||||||||

Data Source: CoinMarketCap API Note: We examine and compare the distance to No Questions Asked during the sample period (21.12.01~22.1.29). During this time, we calculate the convenience yield, which shows that the hybrid stablecoin of TOK fares well with existing global stablecoins Fig. 14. Estimation of ‘convenience yield’11 for stablecoins. |

||||||||||||||||||||||||||||||||||||||||

| In summary, the preliminary results show the feasibility of our proposed solution to overcome initial barriers toward generating DeFi market liquidity via grafting native token with the existing fiat-based stablecoin. Some of the findings underscore the importance of reduced stability, slippage, and robustness property against various shocks as gathered by engineering hybrid features of centralized and decentralized crypto. The target level of stability also allows native protocol token to be eligible for other DeFi protocols for extra network effect. 11 It is identical with the yield, which is the inverse of its price (see [11][12]). |

||||||||||||||||||||||||||||||||||||||||

| In fact, these are the features of the most successful DeFi protocol. For instance, Curve is an AMM platform with many similarities to Uniswap and Balancer but with unique features of accommodating specific liquidity pools of similarly behaving assets like stablecoins or wrapped versions of assets such as wBTC and tBTC. This approach allows Curve to use more efficient algorithms and feature the lowest fees, slippage, and impermanent loss of any decentralized exchange (DEX) on Ethereum. By doing so, Curve can enhance capacity to manage various transactions without incurring huge costs. In other words, it highlights the key features that make future DeFi protocol a successful one. And the preliminary findings in this paper illustrates the feasibility of TOK as a candidate for pairs in the Curve protocol. This possibility underscores the importance of recommending extra stability measures as a prudential guideline for all native protocol tokens before engaging in DeFi transactions. |

||||||||||||||||||||||||||||||||||||||||

| V. SUMMARY AND CONCLUSION | ||||||||||||||||||||||||||||||||||||||||

| In this paper, we set out to introduce a new type of hybrid collateral for specific use of stablecoin in a DeFi setting to reduce the impact of its absence on the system. TOK is a rehashed version of protocol governance token, TON, to promote the ecosystem by addressing specific problems related to most crypto coins. The native protocol token can save resources to expand the DeFi ecosystem by using the stability offered by existing stablecoin in a dynamic setting, by activating the virtuous cycle interaction between token price and liquidity. That is, given the central role of collateral in the DeFi system, existing deficiencies can be effectively addressed in the hybrid context. Technically, we can gradually replace legacy trust with community-based commerce via allowing active role of its native tokens. It is possible to adjust relative weights of pillar stablecoin against native protocol token based on the latter’s predicted volatility over time. This exercise secures collateral base against various shocks that cannot be absorbed in a DeFi setting. The other scenario where we start with less pledgeable assets with significant volatility does not lead to sustainable project since the liquidity generated is based on less secure assets, thus prolonging the project due to extra burden and incentives to maintain liquidity. Liquidity without a profit stream is not sustainable, and it makes a difference to start any project with eligible collateral in the first place. Securing stable collateral backup remains a priority over enhanced reward programs for projects with no clear profit stream. The whole purpose of this approach is to engineer the virtuous cycle for the ecosystem expansion when initial conditions for pledge-able collateral are not satisfied. It differs from the previous attempts in utilizing the already circulated stablecoin to reduce the volatility of the native protocol coin, e.g., TON. Stablecoin as a catalyst for DeFi ecosystem expansion allows us to extract the basic element of trust without invoking heavy regulatory oversight. For instance, the turf war on the payment arena is a significant issue that requires consensus on a global scale. The regulatory concerns can be better dealt with global stablecoins since they provide the most prudential considerations reflecting the concerns of legacy institutions. By securing the basic stability, native crypto can enjoy its unique incentive features to support various projects in the DeFi system. In a related context, securing on-chain DeFi liquidity highlighted some of the features in a monetary system with no central authority. The unique feature of a native crypto token with incentives comes with other limitations that show over time as a trade-off between liquidity and price. Stablecoins help us mitigate this trade-off by allowing us to avoid costs involved in tougher conditions. We can overcome issues related to slippage and segmented liquidity, as well as the overall instability caused by the pooling of highly leveraged liquidity and lack of support from insurance services in the crypto. It also provides the symbiotic link between the legacy and crypto world through dynamic link for global stablecoins to reach out to the infrastructure and synthetic services providers. In this rapidly changing environment, where the key regulatory parameters cannot be determined a priori, the initial conditions for growth and stability in the DeFi ecosystem need to focus on liquidity provision, and improved interoperability with all the necessary infrastructures. Overall, the introduction of TOK type of stablecoins can ease structural problems in the rapidly developing DeFi ecosystem and help the broader crypto world to build trust and stability from the fragile condition. In future studies, the implication of using DeFi stablecoin on interoperability with other protocols and its evolution into synthetic assets will need further studies. Hopefully, these studies will be able to help us better understand DeFi stablecoin. |

||||||||||||||||||||||||||||||||||||||||

| ACKNOWLEDGMENT | ||||||||||||||||||||||||||||||||||||||||

| We appreciate helpful comments by anonymous referees. Thanks to Ms. Grayson who provided excellent data services. Appreciate comments by colleagues at Onther, Inc., especially Mr. Wyatt, who thoroughly read the manuscript and provided insightful comments. |

||||||||||||||||||||||||||||||||||||||||

| REFERENCES | ||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||

Gongpil Choi received his Ph.D. degree in Economics from University of Virginia. Currently, he is the head of the Center for Digital Finance, Korea. |

||||||||||||||||||||||||||||||||||||||||